Overview

Sampling and testing of that sample is used in the planning area and also in the evidential testing areas (planning – for tests of controls in the internal controls section and substantive testing in the evidential testing area - say testing a sample of payments). The style of tests is similar in each place:

- Sampling may be judgemental, created using the firm’s own internal policies (describe in the rationale for sample selection)

- Or in substantive testing areas, the sample size may be obtained using an optional sampling tool, based on performance materiality for that area of the audit

Testing page creation

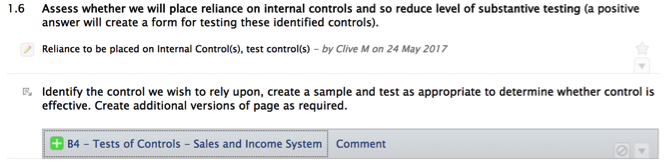

Testing pages are subpages of normal work papers created on an as-required basis. For example here from on a page in the internal controls planning area:

- Selecting reliance to be placed on internal control(s), test control(s) option will create a further workpaper (B4 in this case):

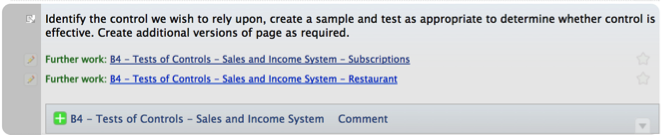

- These testing pages are usually respawners - in other words, the dialog box stays available allowing multiple versions of the testing pages with their own testing tables to be created for say, different types of revenue

- When using multiple versions of a testing page in the same section use different names be used to differentiate the pages as they will both be referenced with the same number in the index - rename say by division:

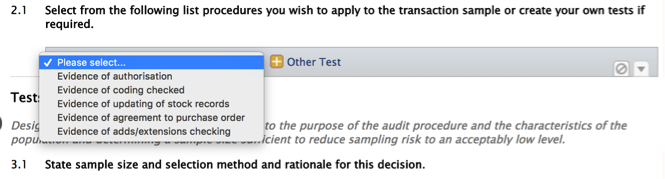

- On the subpage (detailed testing page) enter the details requested to describe the test to be carried out, and select the tests required:

- The columns in the testing table may be edited and added to from the parent page:

- The data columns should correspond with the data being imported from the sample above – either change the import sample to suit the columns or change the columns to match the import

- There is a limit to the number of columns depending on the fit on the page - for extra width landscape may be selected from drop-down – data columns may be added from the please select dropdown, removed or moved

For substantive testing of details see built-in sampling tool.