NZ AS 1 paragraph 6 outlines five objectives that need to be satisfied for the auditor to express an unmodified opinion on service performance (SP) information. These are summarised as follows:

- To understand the process applied by the entity to select what and how to report on its SP;

- To evaluate whether the entity’s SP criteria are suitable (per the financial reporting framework);

- To obtain reasonable assurance about whether the SP information is free from material misstatement;

- To report about whether the SP information is prepared, in accordance with the applicable financial reporting framework; and

- To communicate further as required by the ISAs (NZ) and NZ AS 1, in accordance with the auditor’s findings.

This article will focus on the second point - to help clarify qualitative characteristics and pervasive constraints to better assess the suitability of the service performance criteria (see NZ AS 1 para 22-23).

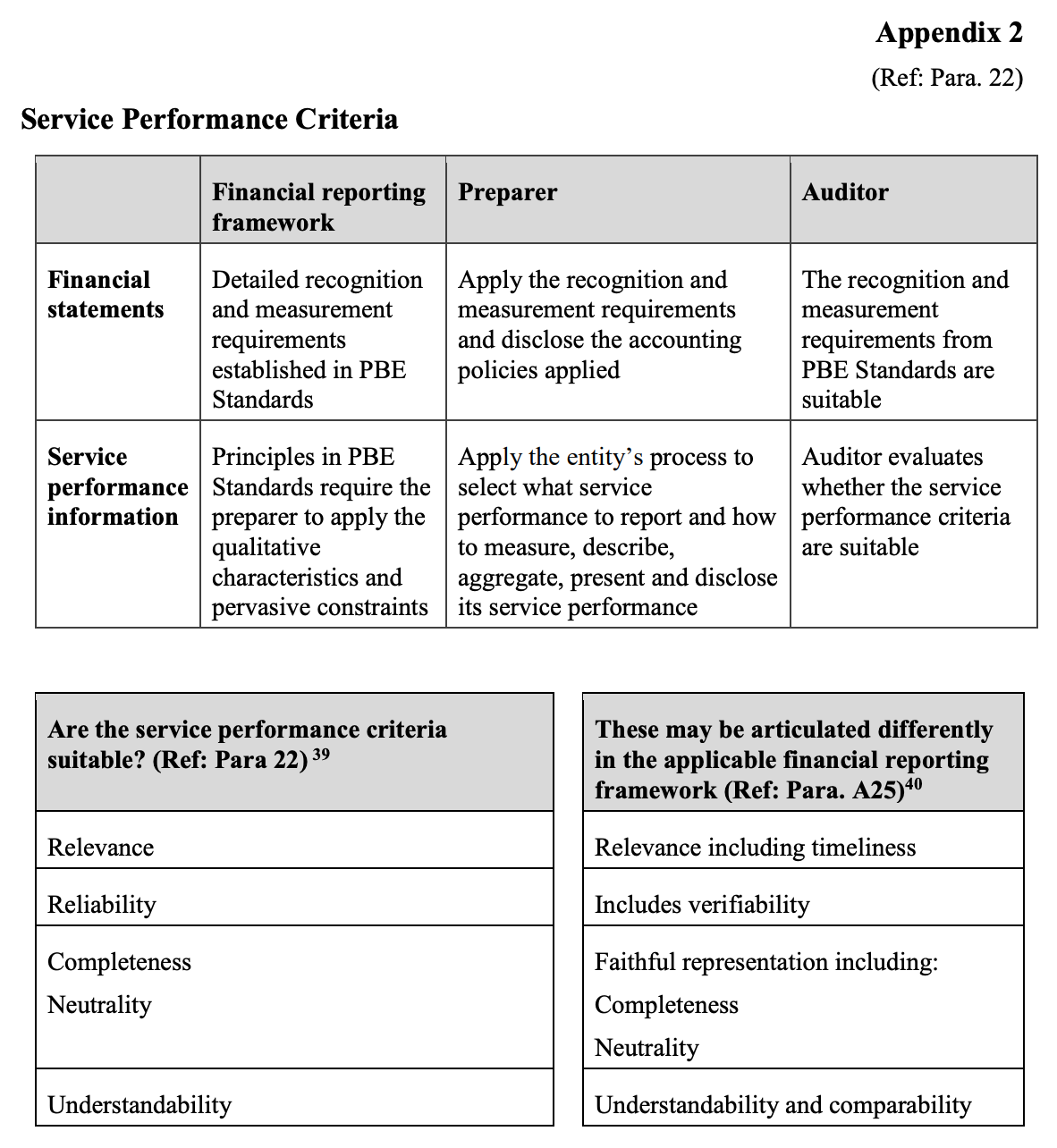

NZ AS 1 Appendix 2 outlines the auditors’ requirements concerning the entity’s service performance criteria:

NZ AS 1 is vague on what constitutes a service performance criterion; this information is found in the PBE conceptual framework (chapter 3).

The entity’s service performance criteria refer to how the entity applies the qualitative characteristics and pervasive constraints of information with consideration to the applicable financial reporting framework, with logical links to the entity’s overall purpose and strategies, and concern to its environment.

Understanding the qualitative characteristics is important because for the auditor to determine whether the criteria is suitable, they need to evaluate the judgements made by the entity in applying the qualitative characteristics and that they are appropriate and have not been significantly affected by management bias.

What are the qualitative characteristics?

(a) Relevance: Strongly linked with judgements about the materiality of information and the appropriate level of groups of data into information. Relevant information assists users in forming assessments about an entity’s accountability for service performance and in making decisions that rely on information about service performance (for example, whether to provide funding to an entity or whether to work with an entity in the pursuit of common goals).

(b) Faithful Representation: Service performance information - which is complete, neutral, and free from material error. Completeness implies that the service performance information presents an overall impression of the entity’s service performance with appropriate links to financial information. Neutrality is the absence of bias. For service performance information to be neutral, it needs to report on both favourable and unfavourable aspects of the entity’s service performance in an unbiased manner.

(c) Understandability: Service performance information should be communicated to users simply and clearly.

(d) Timeliness: Service performance information should be reported to users before it loses its capacity to be useful for accountability and decision-making purposes.

(e) Comparability: Service performance information should provide users with a basis and context to compare an entity’s service performance over time, and where appropriate, against planned performance or the performance of other entities.

(f) Verifiability: service performance information needs to be measurable, capable of independent verification and exclude claims that cannot be substantiated. Verifiability enables users to form judgements about the appropriateness of those assumptions and the method of compilation, measurement, representation and interpretation of the information.

What are the pervasive constraints?

The pervasive constraints on information materiality, cost-benefit and balance between qualitative characteristics are identified in the PBE Conceptual Framework (3.32–3.42). The pervasive constraints exist as preparers (governance, management, accountants) cannot be expected to compile all possible service performance information. Even if they were to, this would create issues such as immaterial information, high compliance costs, and it would be more difficult for users to discern what is essential due to each qualitative characteristic given equal value of importance.

Materiality

Information is material if its omission or misstatement affects the user’s decisions based on the service performance information. Materiality depends on both the nature and amount of the item judged in the circumstances of each entity.

Cost-Benefit

- Financial reporting imposes costs. The benefits of financial reporting should justify those costs.

- Encouraging stakeholders (governance, management, and other users) involved in the preparation to use performance measures specified by the following:

- external benchmarks,

- industry guidance, or

- developed in consultation with intended users (may require less work than internally generated performance measures as external guidance reduces the risk of management bias).

Balance between the Qualitative Characteristics

In some cases, a balancing or trade-off between qualitative characteristics may be necessary to achieve the objectives of financial reporting. The relative importance of the qualitative characteristics in each situation is a matter of professional judgement. The aim is to make an appropriate balance among the characteristics to meet the objectives of financial reporting.

The relationship between Qualitative characteristics and auditor assessment of suitability

The evaluation of suitability is the process of adopting choices and trade-offs made by the entity in determining the most appropriate manner to tell its service performance story. The importance of each qualitative characteristic varies according to the circumstances and the judgements made by the entity in the preparation of the service performance information, which makes it inherently more susceptible to the risk of management bias.

For the auditor to meet the objectives relating to service performance to form an appropriate basis they need to know assumptions made by governance and management in making the service performance criteria, otherwise any conclusion is open to individual interpretation and misunderstanding.

Throughout the process, professional scepticism helps to recognise circumstances that may exist, which can cause the service performance criteria to be biased, incomplete, or otherwise contrary to the qualitative characteristics required by the applicable financial reporting framework.

The auditor will need to assess whether the entity has correctly interpreted the following:

- Applicable financial reporting framework and pre-existing external service performance criteria, including pre-established performance measures and descriptions from guidance,

- Codes, standards, laws or regulation, or

- That it has developed its own internally developed service performance criteria for measuring or describing its service performance.

The entity may follow its own process to identify what and how to report its service performance to implement the applicable financial reporting framework to its circumstances and this is achieved by creating appropriate quantitative measures and descriptions from the framework of the service criteria. The user benefits from this by having service performance information which is more useful for decision making and having reliable outputs that hold the entity to account.

Conclusion

For the auditor to evaluate if the service performance information for the entity is suitable they need to do the following:

- Apply professional scepticism and knowledge of the entity’s working environment, strategies, objectives and outcomes to assess the judgements made by governance and management to ascertain whether there is bias, error or deliberate omission of facts within the service performance criteria,

- Understand how well management and governance in their preparation of service performance information understand qualitative characteristics and pervasive constraints in forming their service performance criteria,

- Use their professional judgement to determine whether these pervasive constraints have compromised the qualitative characteristics of the information presented.

For an overview of NZ AS 1 and how it applies see related article.